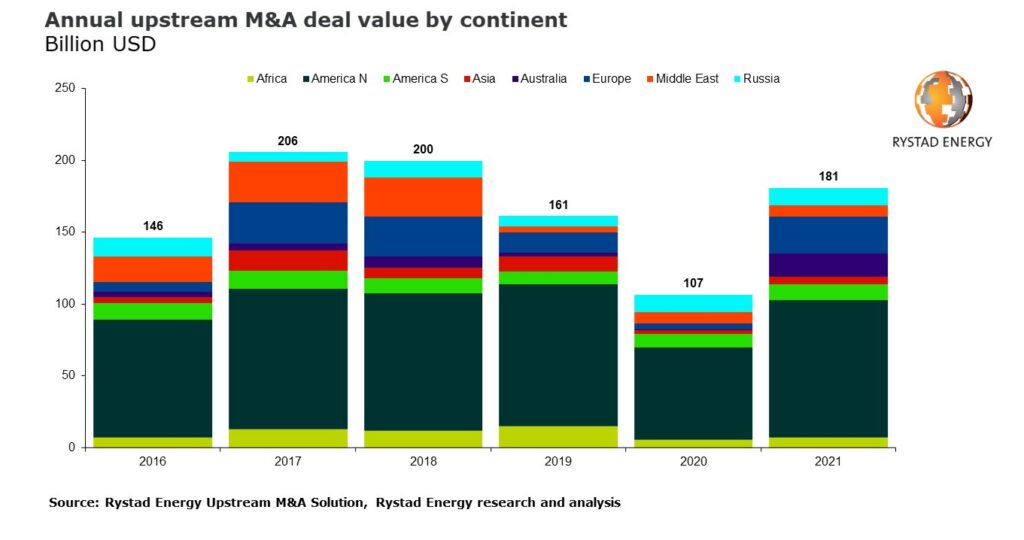

Global upstream merger and acquisition (M&A) deals rebounded to pre-Covid-19 levels in 2021, reaching a total of $181 billion, which is a 70 per cent increase over 2020, Rystad Energy’s research shows. Additionally, the M&A market is likely to stay active for the foreseeable future.

According to Rystad Energy’s report on Friday, the total deal value for 2021 was the highest in three years and almost reached the highs seen in 2017 and 2018 of $205 billion and $199 billion, respectively.

Sellers faced difficulty finding buyers during the downturn in 2020, but that ended last year as big deals made a comeback on high commodity prices and a strengthening market. Deals valued at more than $1 billion accounted for $126 billion, or 70 per cent, of the global total. The share of $1 billion-plus deals rose almost three-fold, with 35 such deals announced in 2021 compared with just 13 in 2020.

Out of the $1 billion-plus deals, 13 were company acquisitions together valued at around $65 billion. Two large Australia-focused mergers – one between Santos and Oil Search and another between Woodside Petroleum and BHP – contributed about $22 billion, while other $1 billion-plus company acquisitions were focused on North American assets.

The share of resources sold in deals shifted in 2021, with gas accounting for 56 per cent of all traded resources, a sizeable jump from the 43 per cent share it had in 2020. Oil accounted for 31 per cent, and natural gas liquids came in at 9 per cent. This shift was primarily driven by the North American acquisitions in 2021 but was also helped by deal activity in other regions.

Ilka Haarmann, a senior analyst at Rystad Energy, said: “With a strong potential deal pipeline, continuous pressure on companies to transform amid a global push to lower carbon emissions while simultaneously delivering profitable oil and gas production, and an average oil price of above $60 per barrel expected for 2022, the upstream M&A market is likely to stay active for the foreseeable future.”

Rystad – breaking down the deals

As detailed by Rystad, company acquisitions totalled $76 billion, around 42 per cent of the global announced deal value in 2021, a drop in share compared with 2020 when purchases accounted for about 57 per cent of the total deal values. The largest company acquisition by deal value was the merger of Cimarex Energy with Cabot Oil & Gas, which was valued at about $17 billion. Following suit with most other North American acquisitions announced in 2021, the deal agreement was signed in the year’s first half. Cimarex and Cabot did not have overlapping asset positions.

The same applied for Appalachia-focused independent Southwestern Energy when it acquired Haynesville-focused Indigo Natural Resources for $2.7 billion and when Paloma Partners acquired Goodrich Petroleum for $480 million. Other U.S. company acquisitions saw the merger consolidate the buyers’ existing portfolio positions.

The largest field acquisitions were Aker BP’s announcement to acquire Lundin Energy’s oil and gas portfolio, valued at about $14 billion, and ConocoPhillips’ acquisition of Shell’s Permian Basin position for $9.5 billion. Field acquisitions in the Permian totalled $19 billion in 2021, accounting for more than half of North American field and license acquisitions, which totalled $35 billion. Russian acquisitions amounted to $12 billion, while in Europe, they clocked in at around $24 billion.

Buyers & sellers

The only peer group with positive net inorganic resource growth in 2021 was public companies, while private players and national oil companies (NOC) divested more resources than they acquired on a net basis. Public companies increased their net resources by about 12 billion barrels of oil equivalent (boe) through acquisitions last year.

However, according to Rystad, there are significant discrepancies between different company segments within this group. The top segment in terms of acquiring resources was public independents growing their positions mainly in North America. Among them were Coterra Energy (formed by the merger of Cimarex Energy with Cabot Oil & Gas), Southwestern Energy, EQT Corporation, Chesapeake Energy and ConocoPhillips. In total, public independents acquired around 34 billion boe of resources in 2021 and sold approximately 21 billion boe, resulting in a net resource growth of about 13 billion boe for public independents.

Among public companies, the majors were the most aggressive in divesting resources in 2021, reducing their collective resources by about 5.5 billion boe on a net basis. The largest inorganic resource reduction among majors was made by Shell, which divested nearly 3 billion boe in North America, 500 million boe in Africa and 200 million boe in Asia. In total, Shell sold around 3.3 billion boe net for more than $11 billion in net proceeds in 2021. ExxonMobil – the major with the second-largest inorganic resource reduction in 2021 – divested net resources of nearly 1 billion boe for a net amount of about $3.8 billion, mainly through sales in Europe and Asia.

Public independents spent more than 75 per cent of the segment’s acquisitions costs on acquiring assets from other public players, including majors, to which around 10 per cent of the total amount spent on upstream acquisitions was paid. Public companies acquired assets worth $125 billion and sold assets for about $114 billion. Private companies in total acquired assets for $45 billion and sold assets for around $46 billion.

Looking ahead

Rystad concluded that the deal pipeline is robust and the upstream M&A market looks set to continue to strengthen, with deals in the U.S. likely to remain a crucial driver of the global deal value. Large sales in other regions may also materialize in 2022, particularly if majors continue to streamline their portfolios.

While resources under development and production can receive high values in the current environment, buyers appear to be more cautious about discovered resources. Without larger changes in the macroeconomic environment, this discrepancy could persist. However, a further steady increase in valuations for producing and under development resources appears unlikely, judging by historical values.

Source: Offshore Energy