The surging demand for infrastructure-related commodities such as iron ore and coal, along with minor bulks such as aggregates, clinker, limestone is likely to help fuel the dry bulk market rally into the third quarter, with freight levels and time charter earnings setting new records.

The dry bulk market has been on a firm footing since the beginning of 2021 and market participants expect the trend to continue in the upcoming quarter.

“I expect the peak [for 2021] has not come yet as the [seasonally firmest quarter] is yet to come,” said a Capesize ship-owning source, adding that healthy demand for sub-Capesize sectors would support the Capesize rates, too.

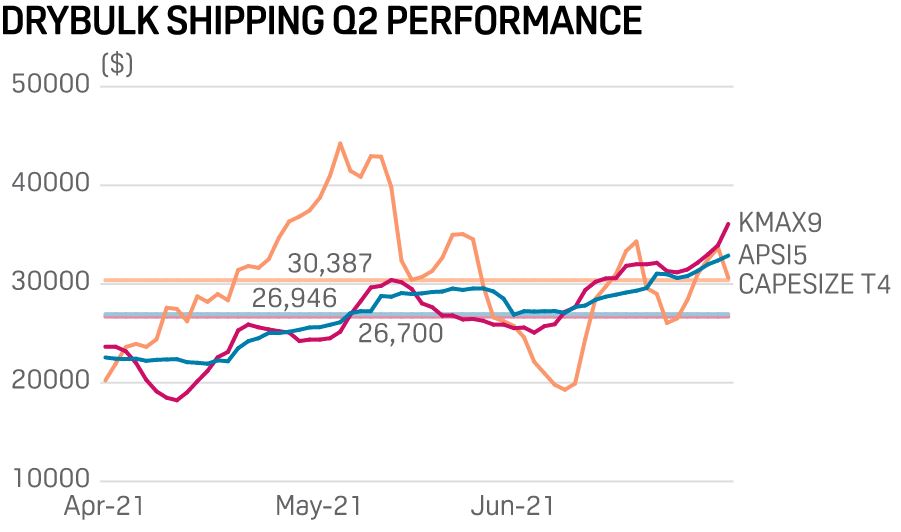

The Platts dual Cape T4 index averaged at $30,387/day and $33,615/day in Q2, basis lower sulfur marine fuel for non-scrubber vessels and scrubber-fitted tonnage separately and registered a record high of $44,233/day and $47,433/day on May 5. Meanwhile, the APSI 5 Index averaged at $26,805/d in Q2, nearly surpassing the Panamax KMAX 9 Index at $26,946/d.

Booming iron ore shipping demand

Major iron ore miners are expected to lift their production in the second half of the year to meet their sales guidance, lifting the outlook for freight rates in H2 2021, especially Q3, on the key Capesize trading routes, according to S&P Global Platts Analytics.

According to the data from Platts’ trade-flow software cFlow, Brazilian miner Vale’s seaborne iron ore exports volumes for H1 2021 was 128.11 million mt, up 10.3% on the year, which showed an annualized run rate of 256.2 million mt, while Vale’s iron ore production guidance for 2021 was 315-335 million mt.

Australian mining major Rio Tinto exported 148.83 million mt during H1 2021, down 8% on the year, with an annualized export run rate of 297.7 million mt. The miner is targeting 325-340 million mt for 2021.

Additionally, the marginal increases from other iron ore export origins like Canada, South Africa, India, and Chile are expected to add to the ton-mile shipping demand as miners there continue to take advantage of the strong iron ore prices.

Gains from grain

The strong grain trade year-to-date has lifted the fortunes of the Panamax and Supramax segments.

Imports of Chinese grains — soybean and other products (corn, wheat, barley, sorghum) — over January-May 2021 came in at 38.20 million mt and 22.30 million mt respectively, up 12.8% and 271.5% on the year, according to the data from Banchero Costa.

Sale of corn from the US to China is also poised to be firm in the coming quarter with 34 million mt outstanding till August, according to shipbroker Howe Robinson.

Unrelenting coal demand

The clamor for coal continued to power the freight market.

According to the International Energy Agency, or IEA, the current coal demand growth for 2021 will be 4.5% on the year, with China accounting for 50% of the increase. But the mounting pressure from China’s National Development and Reform Commission, or NDRC, to curtail inflation remains a roadblock for dry bulk markets. In June, the NDRC had asked provinces to cut power consumption to curb the rising electricity demand.

Elsewhere in Asia, burgeoning coal and freight prices have compelled traders to rejig trade patterns.

With Australian coal not going to China, Indian coal importers are scooping up this coal at a cheaper rate.

“Australian coal sellers have to discount to compete with Indonesian coal. There is a rough freight difference of $15/mt for Australia to India compared with Indonesia to India. Indian buyers are able to purchase Australian coal cheaper than they could have,” said a source with a ship-operator.

Australia surpassed Indonesia as top supplier of coal to India, with a market share of 36.7% over H1 2021 at 39.46 million mt, according to data from Kpler. Most of it moved on gearless ships — Capesizes and Panamaxes –- with Supramax/Ultramax vessels getting a smaller share.

On the contrary, China received more coal tons from Indonesia, Russia, Colombia, and South Africa, with Capesize ships getting a large share.

Persian Gulf spurs market

Notably, low-priced commodities withstood the relentless onslaught from rising freight levels, which were above the product cost. Exports of clinker, limestone, and aggregates from the Persian Gulf saw a rise in H1 2021 compared with the same period in 2020. In fact, limestone exports from Mina Saqr jumped 51.5% on the year.

“The traders are not really very unhappy with these trades. They are still able to sell cargoes at these rates, and they can pass on the costs to the end users. Of course, down the line the commodity boom will fuel inflation, but demand has not yet begun to weaken,” said a shipowner source.

Fleet disarray helping

The coronavirus has disrupted shipping operations extensively.

Crew changes remain a headache for ship-owners as it requires quarantine, and testing protocols. This creates delays and longer wait time at ports.

“We think the vessel’s utilization has yet to be normal [due to COVID-19],” said a Capesize ship-operating source.

“At the same time, however, we do expect a lot of the inefficiencies surrounding the pandemic to fade as we close out the year, slowly releasing pressure from some markets,” said a shipbroker.

Source: Hellenic Shipping